If this is your first visit, be sure to

check out the FAQ by clicking the

link above. You may have to register

before you can post: click the register link above to proceed. To start viewing messages,

select the forum that you want to visit from the selection below.

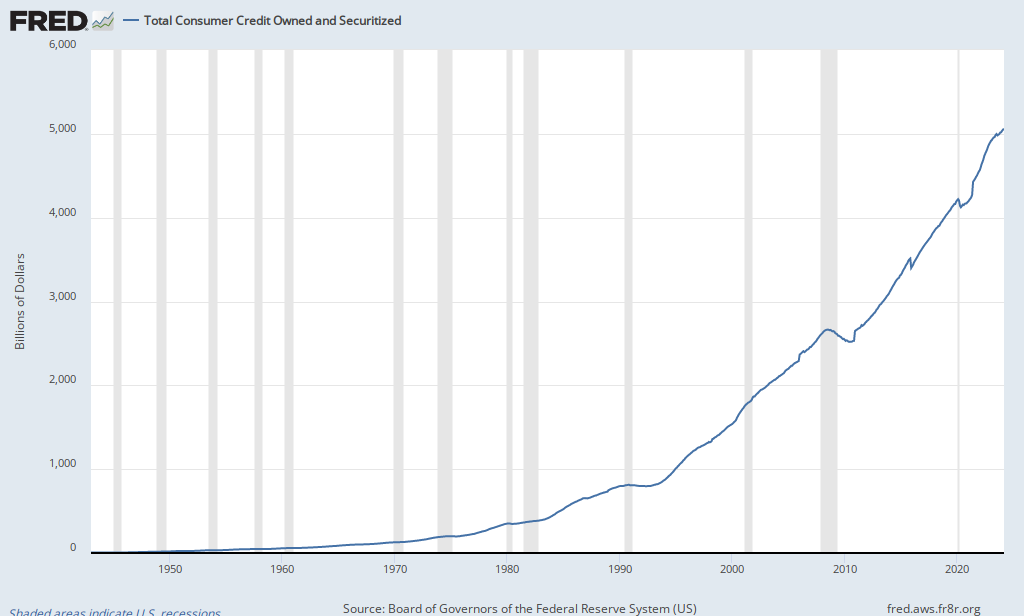

Pretty tricky this time round but low interest rates look a good bet!

Hmmm, let's think about how the housing crash happened in the US:

1) Stock bubble bursts in 2000.

2) The Fed, under the leadership of the wonderful Alan Greenspan lower interest rates dramatically.

3) This kicks off a housing bubble.

There are other aspects like all the ninja loans, lots of bare-naked greed etc. but this is the main causal thread IMHO.

Note that dropping interest rates to zero didn't stop the bubble bursting. In fact it took years and years to recover.

So, IMHO, in NZ, this is playing out too, to some extent. Instead of 7.5% interest rates, we have 4%... and that means you can take on so much more debt...

council legislate that we build average houses at a higher spec. than average wage earners can afford

their solution is to get the top half earners to subsidise the new houses of the lower half

higher end buyers see through so often prefer to renovate an old house in an existing good areaas the whole project hinges on the higher end units for profitability reduced demand there greatly limits the number of projects

hard to see which contradiction is worse

but the current stall in prices

is about as good a solution ss can be expected

can it stay flat for 10 years to allow earnings to catch up?

or is the continual rise in construction costs locked-in?

1. Not true. 2. After the GFC, NZ house prices dropped by what, 7% and then went up sharply. 3. I'm not disagreeing with what you say really, I reckon all this stuff is over priced, but hey, it's been that way for a long time now.

1) You're counter-argument is premised on the fact that just because a significant correction didn't happen in 2007-2009, then it couldn't or won't happen. I suggest you read Nicholas Nassim Taleb's book "The Black Swan". Significant corrections did happen around the globe (Spain, Ireland and various US cities for example). In 2007, the NZ property market was running hot but valuations weren't at obscene multiples of house prices to incomes, which have near doubled. NZ had a unique set of factors that hedged it from global events however it is now significantly more indebted and financial integrated than it was back in 2007, meaning financial contagion will have a greater effect next time there's a global financial event.

If you're a student of financial history then you will know that no two corrections (crashes) or booms (bubbles) are the same. There's always a different set of financial conditions and circumstances, pressures, catalysts, and outcomes. Just because the GFC had a rather limited effect on NZ, it doesn't mean next time will be the same.

2) Sharp increase after the GFC? Let's diagnose that argument for a second.

a) The GFC happens (primarily a US-centric event).

b) The US Federal Government via the US Treasury intervenes with its TARP bailout in order to immediately stabilise the economy.

c) In order to combat deflationary forces, the US Federal Reserve undertakes the greatest financial accommodation programme in the entire history of man, cutting the Fed Funds rate from 5.25% down to 0.25%, in addition to several Quantitative easing programmes which increased their balance sheet from $800bn to $4.5 trillion.

d) The other major central banks (ECB, BOJ and SNB) followed suit and collectively increased their balance sheets to $21 trillion.

f) In addition to the above, in the last few years, China alone has created roughly 50% of the world’s new debt growth.

e) Almost all of this financial accommodation flowed through to the financial sector creating inflation in Asset Prices (stocks, bonds, real estate, commodities etc). Very little of this liquidity flowed through to the intended Joe Public in order to boost their personal income/wealth and encourage a consumption lead recovery.

From the narrow perspective of the Auckland property market, yes its easy to say that the GFC had a relatively miniscule impact and that property prices will surely continue to infinity on the basis of the "fundamentals".

Yet if one takes a much larger viewpoint of the financial world then it becomes readily apparent that these fundamentals are simply symptoms of much larger events, namely the greatest period of monetary expansion (experimentation) in the entire human history.

Let's take stock for a moment and consider where we currently are:

a) We are now 96 months into a recovery (third longest on record), interest rates are still extremely low, inflation remains muted and the central bank’s balance sheets are still growing. The world is at record levels of indebtedness with 327%+ Global Debt/ Global GDP.

b) Wage/Income growth remains stagnant and unemployment statics (while proving strong) appear unrealiable. For instance, much of the job growth in the US is due to part-time jobs as individuals are loading up on their second or third part-time job in order to get by. A large proportion of the US economy is effectively broke and has limited prospects for employment.

c) Financial Assets remain at all-time highs (and near record relative highs) due to financial accommodation (particularly low interest rates) encouraging corporates to buy back their own stock. This adds near zero value to the wider economy, but does benefit their shareholders.

d) Some financial commentators speculate that rates can never “normalise” because governments and corporations could never effectively service their debts. The US in particular would have trillion dollar interest payments at a normalised rate of say 5%.

e) It's becoming increasingly evident that the financial accommodation can no longer continue, at least at the current pace. The European Central Bank for instance is running out of German Sovereign Bonds to buy (there's only several months inventory left). The Swiss and Japanese Central Banks have now already transitioned to purchasing stocks which is arguably one of the most destructive forms of central bank intervention ever conceived. Experiments in cutting interest rates below the zero bound have been met with failure and are creating industry wide distortions as sectors like insurance, wealth management and banking struggle to exist in a negative interest rate environment.

3) Yes it has been this way for a long time. The world has become exponentially more indebted since approximately 1974, with some hiccups (deleveraging cycles) along the way.

Will it always be this way? Who know but it appears that we are struggling to reach escape velocity. Debt growth is continuing to outpace real economic growth, which itself is continuing to decline as each new dollar of debt yields less and less gross. This means ever increasing leverage, i.e. borrowing from ones future to spend (subsist) in the present. From a systems perspective this is completely unsustainable.

What do I think will happen? Hard deleveraging. The closet proxy to this scenario is 1929, and the 1999-2000 Dot Com Crash, albeit on a much wider, globalised scale.

Okay, lets get back to basics, prices go up and down due to supply and demand curves.

And many factors affect demand and supply.

Prices ARE down 150k now, on the Shore, demand hammered by lack of Chinese and Bank Credit Rationing (LVR a red herring).

Nothing is selling.

But as Dean says, most people will sell at a reduced price instead of the Bonanza prices of mid 2016, but wont take a big hit as they dont have to sell.

Listings rose to dizzy heights as properties did not sell, they have come off market now and people have stopped listing as the crazy prices are not their.

We are now, close to the bottom, maybe a bit more fall around election time and Christmas as some people do have to sell.

But slow grind back in 2018 from this low, as the factors that support demand reassert themselves.

Watched a film the other day, heavy use of drones doing all sorts of things, this is important to this and other threads, something I have mentioned before.

The age of terrorism has just begun, they will get their hands on this stuff and wont be delivering Pitza's.

Travel tourism will become a thing of the past for most parts of the world.

Auckland is a global city safe haven.

An Armageddon of some sort will come, and massive price rises in Auckland and satellite cities, will happen, just a question of when.

Look where we are and what we have.

What was the film? I have a friend who is a genius programmer and he started a business developing the operating software for very complex drones. What he showed me backs up your statement.

Okay, lets get back to basics, prices go up and down due to supply and demand curves.

And many factors affect demand and supply.

Prices ARE down 150k now, on the Shore, demand hammered by lack of Chinese and Bank Credit Rationing (LVR a red herring).

Nothing is selling.

But as Dean says, most people will sell at a reduced price instead of the Bonanza prices of mid 2016, but wont take a big hit as they dont have to sell.

Listings rose to dizzy heights as properties did not sell, they have come off market now and people have stopped listing as the crazy prices are not their.

We are now, close to the bottom, maybe a bit more fall around election time and Christmas as some people do have to sell.

But slow grind back in 2018 from this low, as the factors that support demand reassert themselves.

Supply/demand.. Supply we can generally forecast however almost all demand is a function of both credit availability and affordability as highlighted in your own argument. Your argument assumes that these will not change. I suspect that this is unlikely to hold true given the events (at the Central Bank level) that I pointed out above.

If interest rates do normalise (to 7%-8%) then house prices will likely contract as borrowers are squeezed. Events like the GFC affect credit availability (e.g. a credit crunch driving a premium for offshore funding).

Even if borrowers hold on and weather the storm, as I've pointed out above there is unlikely to be another massive surge in liquidity (financial accommodation) as the Central Banks can't keep printing money (quantitative easing) as eventually they run out of stocks and bonds to buy (i.e. they own everything). There is an upper-bound.

What you've seen is the greatest central bank experiment in financial accommodation ever, its had limited success and has limited prospects to continue. As such one can only deduce that the best times for Global Asset Growth (e.g. house price inflation) have come.. and been.

I think we have been down this track of conspiracy theory and over dramatization of reality enough on this thread.

Auckland fundamentals are very very good, top end Chinese money is still coming in, Europeans and wider asia still coming here buying property.

Banks still have to lend to make money and decades of low / moderate interest rates on the cards still.

Demand late last year was hammered by several things happening at the same time, not a perfect storm but enough, prices have moderated but that's about where the story ends.

I think we have been down this track of conspiracy theory and over dramatization of reality enough on this thread.

Auckland fundamentals are very very good, top end Chinese money is still coming in, Europeans and wider asia still coming here buying property.

Banks still have to lend to make money and decades of low / moderate interest rates on the cards still.

Demand late last year was hammered by several things happening at the same time, not a perfect storm but enough, prices have moderated but that's about where the story ends.

Thanks for your beige opinions there Paul.. judging by your submission to the RBNZ you are clearly have a sound knowledge of the financial system not to mention well articulated arguments around macro-prudential affairs.

Tweet

Tweet

Comment